The Workday - A16z Debate Has Five Smart Takes. Here's What They're All Missing.

A platform shift is underway in enterprise HR technology. Most serious observers agree on that much. What they disagree on, sometimes sharply, is what it means, how fast it happens, and who wins.

Over the past week that debate has played out publicly in five contributions worth reading together. Joe Schmidt at a16z argued that Workday is facing the same disruption it once delivered to PeopleSoft, and called for founders to build an AI-native replacement. Thomas Otter, a veteran HR tech analyst and partner at Acadian Ventures, pushed back, arguing the challenge isn’t architectural but visionary: we don’t yet have a compelling new model for how HR should work. Anita Lettink, a global payroll and HCM implementation expert with two decades of advising enterprises on exactly these systems, went further, making the case that the conditions that made Workday possible no longer exist and that the real opportunity is to build for the workforce of 2035. Jerome Gouvernel, CEO of datascalehr, made the most provocative argument: that ERPs as a category may not survive the AI shift at all, displaced not by a better ERP but by something that answers the same need entirely differently. And Andy Turnbull, Head of People at Bolt and co-founder of advisory firm Wave1, offered the practitioner’s read: stop debating whether Workday survives, start asking what role it plays in a stack that no longer revolves around it.

All five are worth your time. All five are partly right. And taken together, they still leave the most important questions unanswered.

I want to do something nobody else in this conversation has done yet: look at each argument on its merits, say where I agree and where I think the analysis falls short, bring a data lens that’s been missing entirely, and point to where I think the real displacement threat actually comes from. I have a specific vantage point here. I was in this market when PeopleSoft was built and when Workday emerged from its ashes, and I’ve spent the past decade tracking more than $65 billion in Work Tech funding across 60-plus categories. That history and that data are what I’m adding to this conversation.

What the debate gets right

Schmidt’s core diagnosis is accurate. Workday cannot become AI-native without starting over, and starting over is the one thing a public, installed-base company can’t do. The Flex Credits story looks like commercial traction until you read it carefully. Booking AI revenue and running core HR workflows through agents in production are very different things. The architectural pressure is real, and Workday knows it.

Thomas Otter is right that architecture alone won’t decide this. Building a slightly better Workday on a cleaner stack is achievable. Building a genuinely new vision for how HR should work, one that is impossible to deliver on existing technology, is the harder and more important challenge. That vision doesn’t exist yet.

Anita Lettink is right that the conditions that gave rise to Workday no longer exist. The greenfield enterprise market no longer exists. Procurement cycles can consume a startup for months without a dollar of revenue. The trust deficit facing any new entrant is real. It took Workday years to earn enterprise credibility, even with Duffield and Bhusri’s reputations behind it.

Jerome Gouvernel is right that the more interesting question isn’t who rebuilds the ERP but whether the ERP category survives the shift at all. His ice industry analogy is the most intellectually honest framing of what AI could eventually do to encoded business logic. The domestic refrigerator didn’t beat the ice plant; it made the entire ice industry obsolete by answering the same need in a different way.

Andy Turnbull is right that Workday’s API credit metering is the thing CHROs should be watching most closely right now. The more you integrate Workday with the rest of your stack, the less budget you have for the AI agents that are supposed to deliver ROI. More than a pricing quirk, it’s a strategic choice about lock-in at exactly the moment the market wants modularity.

Where the analysis falls short

Here's where I part ways with all of them.

Jerome’s refrigerator is elegant. But domestic refrigerators didn’t have to calculate payroll across 47 jurisdictions, comply with ERISA, pass a SOC 2 audit, or survive a benefits eligibility dispute before a CHRO would plug them in. What remains in the substrate, as Jerome correctly identifies, is governance, compliance, storage, and security. But who owns that substrate is determined by domain expertise and regulatory credibility, not by who has the cleanest LLM integration. Jerome builds the case for the moat and stops just short of following it to its conclusion.

Schmidt's "always-on compliance" feature has an agent that monitors regulatory changes and drafts configuration updates, which reads as a bullet point to someone who has never had to explain to a CHRO why payroll ran wrong in Germany. And remember: Workday doesn't even run native payroll in Germany. That's an integration. Compliance in large enterprise HR isn't a monitoring problem. It's an accountability and liability problem. Someone must be held responsible when it goes wrong. Current AI systems face both technical and regulatory limits on explainability and auditability that agent velocity alone can't overcome. This is the constraint that Silicon Valley has underestimated about HR for 30 years. This debate underestimates it again.

There’s also a gap in Schmidt’s competitive framing that nobody else in this conversation has addressed directly. Workday isn’t just an HRIS. It is the leading enterprise ATS. It runs benefits, workforce management, and learning at scale. It has native payroll in the US, Canada, the UK, and France, and relies on integrations everywhere else, which is itself a signal of how hard the problem actually is. A challenger doesn’t just need to replace core HR; they need to replace an interconnected platform where each module carries its own implementation complexity, compliance requirements, services ecosystem, and switching costs. The ATS alone involves OFCCP compliance, EEO reporting, data residency requirements across jurisdictions, and integration with every downstream onboarding and payroll workflow. Replacing Workday means replacing all of that simultaneously, or threading a needle of partial displacement that Workday’s own bundling strategy is specifically designed to prevent.

And across all five pieces, nobody has asked what the actual capital data says about who is positioned to win.

What nearly a decade of data shows

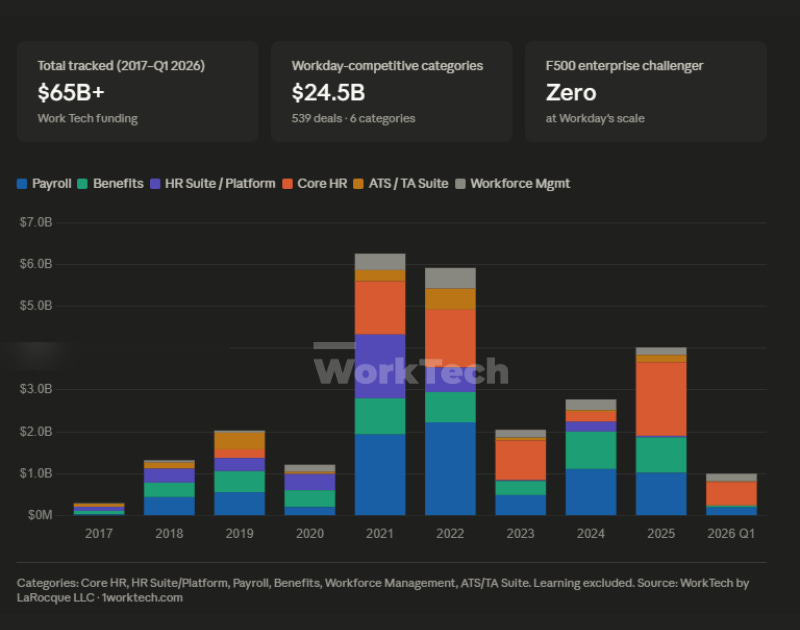

WorkTech has tracked HR and Work Tech funding since 2017, $65 billion across more than 2,400 deals in 60-plus categories. That dataset tells a story that the current debate is missing.

Across the six categories that map directly to Workday’s core product footprint, Core HR, HR Suite/Platform, Payroll, Benefits, Workforce Management, and ATS, the market has deployed $24.5 billion across 539 deals since 2017. That’s more than a third of all Work Tech capital tracked over that period, flowing into exactly the categories where a Workday challenger would need to compete.

The 2021 peak alone was $5.7 billion across 83 deals, the year Rippling, Personio, HiBob, and Paycor all raised landmark rounds. Serious companies. Growing companies. Winning the mid-market. None of them is an F500 enterprise HRIS replacement at Workday’s scale.

Post-peak, investment dropped sharply to $1.9 billion in 2023 before recovering to $3.8 billion in 2025 as Rippling’s Series G, iSolved, and Deel continued scaling. The capital has been consistent. The enterprise ceiling has held.

The ATS data makes the point even more clearly. Seventy deals totaling $1.7 billion since 2017, and the largest single transaction was a 2019 private equity recap of Jobvite (now Employ), an existing player restructuring, not a new entrant breaking in. Greenhouse, SmartRecruiters, and Ashby are genuinely strong products, broadly respected in the market. None of them is touching Workday’s position at the F500 scale. This is the category Schmidt doesn’t appear to have on his radar at all, and it’s one of Workday’s most defensible positions.

Nearly a decade. $24.5 billion across Workday’s core footprint. The enterprise ceiling has held every time. That is not a funding gap. That is a domain signal.

The Q1 2026 M&A data reinforces it from the other direction. WorkTech tracked 40 transactions across 10 countries in that quarter. The dominant pattern doesn’t reflect disruption from outside; it’s deliberate capability acquisition from within. Twelve of the 40 transactions involved HCM platforms acquiring adjacent capabilities: compliance infrastructure, EOR, and country-specific payroll services. Remote acquired Atlas and Easop in the same quarter. Payoneer acquired Boundless. SD Worx added payroll in France and Italy. Global payroll platforms are building the full employment infrastructure stack through acquisition. Incumbents hardening positions, not startups breaking in.

The single most strategically interesting data point in the entire dataset isn’t a venture round. It’s the largest deal in the Workday-competitive categories in Q1 2026: Vensure Employer Solutions, $450 million in debt funding. Not venture capital chasing a thesis. Operational capital scaling a business that already runs payroll, compliance, and employment services at scale across jurisdictions. That’s the signal worth watching, and it points directly to where the real threat may come from.

Where the real displacement threat actually lives

The next credible challenger in enterprise HCM is almost certainly not emerging from the seed-stage cohort any VC is funding today. The capital data support that conclusion across nearly a decade of evidence.

The more credible path runs through the EOR and PEO space. Vensure has the compliance playbook, proven M&A discipline, global infrastructure, and market credibility to extend well beyond SMB and mid-market if they choose to. They’re already operating at scale where the hard problems actually live. A company like Vensure starts from a position of solving this problem at scale across jurisdictions. That’s a fundamentally different risk profile than starting at zero with a clean codebase and an impressive demo.

Andy Turnbull’s SaaS-to-SaS framing applies directly here. Replace the people with agents, and the unit economics of a services-first model change entirely. Deel already demonstrates the pattern: it looks like a SaaS company, but is operationally a services company: employer of record, global payroll, HR operations at scale. The companies best positioned to win in the next wave are those that combine operational depth with the technical capability to automate it. That’s not a founder story. That’s a scale story.

The second candidate is an adjacent acquirer from payments, benefits, or another regulated domain who brings earned trust and operational discipline alongside capital and ambition. The Q1 M&A data shows exactly this pattern already playing out on a smaller scale. It will move upstream.

What this means if you're making decisions today

The platform shift is real. The direction is clear. The timeline is not.

If you’re a CHRO navigating a Workday renewal right now, the question worth asking isn’t whether to wait for an AI-native replacement. It’s about positioning your infrastructure to take advantage of the shift when it matures, without betting your workforce's employment relationship on a vendor who hasn’t yet earned the right to run it.

If you’re a vendor or investor in this space, the signal in the capital and M&A data is consistent: the enterprise ceiling has held against pure technology plays for nearly a decade. The next move will be made by someone who combines domain credibility with technical capability, not someone who leads with the technology and acquires the domain knowledge later.

I’d welcome multiple thoughtful challengers to Workday and the legacy HCM platforms. I’d welcome the vision Thomas Otter is asking for, one that genuinely rethinks how work gets done. I’d welcome the approach Anna describes, building for the 2035 workforce with compliance baked in from the start, not bolted on after the fact.

The direction of this market is not in doubt. What’s in doubt is the timeline, the path, and the identity of the winner. On all three, the data points somewhere different than the current debate suggests.

George LaRocque is Founder of WorkTech, a market intelligence and advisory firm covering the HR and Work Tech ecosystem. The Q1 2026 Global Work Tech M&A Update and VC Update referenced in this piece are available at 1worktech.com.

Domain credibility with technical capability is true for individuals and organizations right now. It is also true that what we see moving forward as differentiation is the intersection of trust and backstopping liability. This is the key shift in the "tech enabled services" conversation - the business model of software is shifting/expanding again in this world where we aren't just selling software but outcomes. In the HR tech space the rubber meets the road in payroll/payment and the business model expands against that question.

Really enjoyed this analysis. TY